RMD Age Changes. What Does it Mean for Me? | Financial Advisor | Christy Capital Management

Today, were talking about the RMD ages. RMD is the required minimum distribution the IRS makes you take as distributions from your traditional IRA or traditional TSP account. They've made some changes over the last year or so.

The RMD age used to be 70 1/2, so if you were born prior to July 1, 1949, that would have been your RMD age. Under the Secure Act, the RMD age changed to age 72. So if your birthdate is between July 1, 1949 and 1950, your RMD age will be 72. Under the new Secure Act 2.0 that was passed in December 2022, they increased the RMD age to 73, so if you were born from 1951 to 1959, that’s your RMD age. And for those born 1960 or later, the Secure Act 2.0 pushes the age to 75.

This is a way for the IRS to ensure that retirees can’t defer their gain forever. They require you to take a minimum amount out and therefore will require you to pay taxes on it. They’ve also reduced the penalty where it used to be a 50% penalty if you did not take your RMD by the deadline and now they’ve reduced it to 25%, and in some cases down to 10% if you can correct the problem within two years.

They also changed the rule beginning in 2024 where you won’t have to take an RMD from Roth 401(k)s or Roth TSPs. This will make it a lot more like Roth IRAs that do not require RMDs at all.

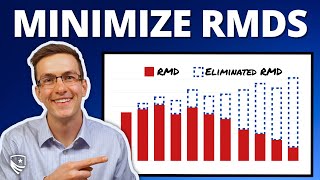

So does this give you any planning opportunities based on these changes? I say that it does. If you’ve got a rather large TSP account and you allow it to continue to grow all the way up to age 75, that balance can get rather large by that date. When they make you take out a required minimum amount, it can be a pretty large amount, which can push you up in the tax bracket that you may not want be in. Based on your other income and what the current tax brackets are at that time, RMDs can push you up into a tax bracket that you wouldn't ordinarily be in and may not want to be in. So what you can do about that before age 73 or 75, is to do tax planning and start shifting some money from traditional to Roth with the goal of arriving at age 73 or 75 with a certain amount of traditional money, but not a huge amount of traditional money.

Most people feel that the goal is to have as much money as you can and more money is usually better. That's a great goal with the caveat that you want to hold your money in the best account. If you’re holding it in a Roth account, it is no longer subject to taxation as long as you play by the two rules of no withdrawals on your gains until your over 59 1/2, and you've had the Roth IRA for five years.

Growing a traditional account can generate a problem when you show up at your RMD age and they make you take out a bunch of money. Once you start taking your RMDs, it is in the ballpark of taking 4% out of your traditional balances. At that rate for every million dollars you have, that’s about $40,000 that they require you to take out.

So, maybe you have 500,000 or $600,000 now at age 59, but by 75 you can have two or three million dollars depending on how much you spend and how aggressive you are invested. Putting a bridle on the traditional account, by shifting money to Roth can be wise tax planning for some people. Now, make sure you’re consulting someone oneonone for your personal situation, but generally speaking having more money in Roth, as opposed to more money in traditional can make sense once you hit your RMD age.

The fact that these ages have been pushed out, gives you more time to be doing the Roth conversions. One of the planning ideas that we go over with clients is figuring out how much you can Roth convert each year so that you show up at your RMD age with an appropriate amount of Traditional money. For some people that may be having zero in your traditional account. Others that are charitably minded may want to have some traditional money so they can take it advantage of the qualified charitable distributions and get an extra tax break when you hit age 70 1/2. But, that’s a discussion for another video.

The information provided is not intended as tax or legal advice. Figures shown are for illustrative purposes only furthermore, the information nor the illustrations provided may not be used to avoid any tax penalties. This content represents the general views of Christy Capital Management and should not be regarded as personalized investment advice Nothing herein is intended to be a recommendation. The opinions expressed are subject to change without notice. Retirement Benefits Institute, Inc., and a portion of its contents merged with Christy Capital Management Inc. Brandon Christy, former President of Retirement Benefits Institute, is also the current President of Christy Capital Management, Inc, a registered investment adviser.