Why is the Age 59.5 so Important? | Financial Advisor | Christy Capital Management

What’s so important about the age 59 1/2? If you’ve been researching retirement planning, you've probably noticed the age 59 1/2 come up often. There are a few reasons for that.

At age 59 1/2, retirement savers can begin making penaltyfree withdrawals from retirement accounts such as TSPs and IRAs. Remember they are penaltyfree withdrawals, but if they are traditional accounts, you still have to pay taxes.

If you have a Roth TSP or Roth IRA, you can make taxfree withdrawals after the age of 59 1/2. For Roth TSP, no matter what, they will be taxfree. However, for Roth IRAs, you have to be 59 1/2 or over and you have to have had a Roth IRA account for at least five years. Not necessarily that specific Roth account, you just need to have had a Roth account opened up somewhere at least 5 years ago. Even if you don’t meet the fiveyear rule, you can still access your contributions or your Roth conversions from a Roth IRA within the five years. You just can’t touch the growth until after five years.

Another thing is that the TSP allows you access to your money. You can either take a penaltyfree withdrawal like we’ve discussed or you can roll your account into a traditional IRA. This opens up more options for you. There are other investments you can choose from, and other planning things you can do like doing Roth conversions.

In an IRA, you can do Roth conversions. In the TSP, you cannot do them. A Roth conversion is where you take some traditional money and you move it to Roth and go ahead and pay the taxes now. The thought process is if you think the tax rate is lower now than it will be, then you would go ahead and start doing some Roth conversions. The TSP doesn’t let you do that. In an IRA, you can do it. And at 59 1/2, you gain access to where you can move your TSP out. So if you’re still working at 59 1/2, you have access to your TSP. If you have already retired, let’s say at age 57, you have access to your TSP and can move it out then.

So what are some of the reasons why one might want to move their TSP out to do an IRA? The TSP is somewhat limited. They have opened up the mutual fund window which now has thousands of choices but now that’s almost too many choices that you have to research yourself. It’s also very cumbersome inside the TSP to access the mutual fund window. You have to move money from the regular TSP into the mutual fund window, and then you have to invest it. If you need to take a distribution, you have to divest it and move it back to the regular TSP. So it’s a bit cumbersome.

Another reason to move money out is if you want help with your financial planning or tax planning. Like other things in life, can you do this on your own? For many people, they can. For instance, I can change the oil in my car. I can file my own tax return. But, I choose not to because I think there is value in having somebody really good at it do it for me.

Another reason why people should move their TSP out is the beneficiary loophole problem in the TSP. The TSP only allows you to leave money to a beneficiary at your death. If you leave it to someone that is not your spouse, they would roll the money out into it inherited IRA and everything would be fine. If you leave it to your spouse, they can open up a TSP beneficiary account. Everything is still normal. The problem comes when your spouse dies, the TSP no longer allows them to roll that money into someone else’s inherited IRA. Instead, that secondary beneficiary has to take a full distribution, so if it’s traditional, it's going to be fully taxable all in one year. That could be a huge problem.

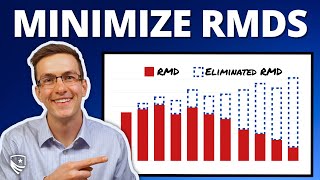

Another reason people are moving money out of the TSP is to do the Roth conversions that we talked about. If you think income tax planning is important, then Roth conversions will be important for you. TSP doesn’t allow it. I would even go as far as saying if you were a federal employee with a pretty healthy pension and getting Social Security and have $500,000 or more in your TSP, you’re very likely going to have tax issues. The TSP balance will grow over time, and when you have to start taking required minimum distributions at age 73 or age 75, they can sometimes push you into higher tax brackets.

The information provided is not intended as tax or legal advice. The figures shown are for illustrative purposes only. Furthermore, the information nor the illustrations provided may not be used to avoid any tax penalties. This content represents the general views of Christy Capital Management and should not be regarded as personalized investment advice Nothing herein is intended to be a recommendation. The opinions expressed are subject to change without notice. Retirement Benefits Institute, Inc., and a portion of its contents merged with Christy Capital Management Inc. Brandon Christy, former President of Retirement Benefits Institute, is also the current President of Christy Capital Management, Inc., a registered investment adviser.