The easiest way to skyrocket your YouTube subscribers

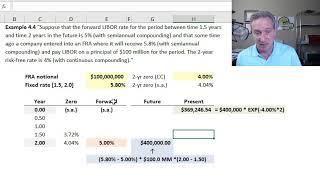

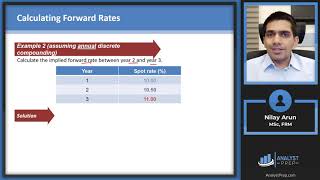

Forward rates are implied by zero rates (FRM T3-11)

[my xls is here https://trtl.bz/2HMQkUU] Forward rates link two zero (aka, spot) rates by ensuring your expected return is the same between two choices: (1) invest at the longerterm spot rate versus (2) invest at the shorterterm spot rate and "roll over" into the implied forward rate. This is an implied forward rate that ignores other factors such as liquidity preference. Discuss here in our FRM forum: https://trtl.bz/2VH93eY.

Recommended