The Greeks Explained - How to Trade Options

Check out my entire playlist on Trading Options here:

• How to Trade Options

Like, Comment, and Share my videos!

SUBSCRIBE HERE http://bit.ly/BroeSubscribe

LET’S CONNECT

Instagram @JakeBroe / jakebroe

Twitter @Broe_Jake / broe_jake

Watch My Other Videos Here

★ How to Swing Trade Stocks (THE BASICS)

• How to Swing Trade Stocks (THE BASICS)

★ My $25,000 Brokerage Account Challenge (2021)

• My $25,000 Brokerage Account Challeng...

★ How to Trade Options (Buying Call Options)

• Buying Call Options Explained How t...

================

The Basics of The Greeks

Greeks encompass many variables. These include delta, theta, gamma, vega, and rho, among others. Each one of these variables/Greeks has a number associated with it, and that number tells traders something about how the option moves or the risk associated with that option. The primary Greeks (Delta, Vega, Theta, Gamma, and Rho) are calculated each as a first partial derivative of the options pricing model (for instance, the BlackScholes model).

Delta

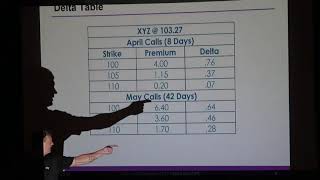

Delta (Δ) represents the rate of change between the option's price and a $1 change in the underlying asset's price. In other words, the price sensitivity of the option is relative to the underlying asset. Delta of a call option has a range between zero and one, while the delta of a put option has a range between zero and negative one. For example, assume an investor is long a call option with a delta of 0.50. Therefore, if the underlying stock increases by $1, the option's price would theoretically increase by 50 cents.

For options traders, delta also represents the hedge ratio for creating a deltaneutral position. For example if you purchase a standard American call option with a 0.40 delta, you will need to sell 40 shares of stock to be fully hedged. Net delta for a portfolio of options can also be used to obtain the portfolio's hedge ration.

A less common usage of an option's delta is it's current probability that it will expire inthemoney. For instance, a 0.40 delta call option today has an implied 40% probability of finishing inthemoney. (For more on the delta, see our article: Going Beyond Simple Delta: Understanding Position Delta.)

Theta

Theta (Θ) represents the rate of change between the option price and time, or time sensitivity sometimes known as an option's time decay. Theta indicates the amount an option's price would decrease as the time to expiration decreases, all else equal. For example, assume an investor is long an option with a theta of 0.50. The option's price would decrease by 50 cents every day that passes, all else being equal.

Theta increases when options are atthemoney, and decreases when options are in and outofthe money. Options closer to expiration also have accelerating time decay. Long calls and long puts will usually have negative Theta; short calls and short puts will have positive Theta. By comparison, an instrument whose value is not eroded by time, such as a stock, would have zero Theta.

Gamma

Gamma (Γ) represents the rate of change between an option's delta and the underlying asset's price. This is called secondorder (secondderivative) price sensitivity. Gamma indicates the amount the delta would change given a $1 move in the underlying security. For example, assume an investor is long one call option on hypothetical stock XYZ. The call option has a delta of 0.50 and a gamma of 0.10. Therefore, if stock XYZ increases or decreases by $1, the call option's delta would increase or decrease by 0.10.

Vega

Vega (v) represents the rate of change between an option's value and the underlying asset's implied volatility. This is the option's sensitivity to volatility. Vega indicates the amount an option's price changes given a 1% change in implied volatility. For example, an option with a Vega of 0.10 indicates the option's value is expected to change by 10 cents if the implied volatility changes by 1%.

================

#OptionsTrading #OptionsGreeks #TheGreeks

================

DISCLAIMER:

This video is for entertainment purposes only. I am not in any way acting as an agent or representative of the Department of Defense or United States Federal Government when presenting this information. I am not a legal or financial expert or have any authority to give legal or financial advice. While all the information in this video is believed to be accurate at the time of its recording, realize this channel and its author makes no express warranty as to the completeness or accuracy, nor can it accept responsibility for errors appearing in this video.