Get YouTube subscribers that watch and like your videos

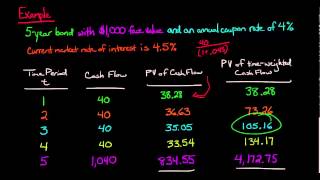

Understanding credit spread duration and its impact on bond prices

M&G’s Mario Eisenegger explains the basic dynamics of credit spread duration, a measure of how sensitive a bond’s price is to movements in credit spreads

The video highlights the two drivers of credit spread duration; the coupon and maturity. Using some examples, we look at how coupon size and maturity periods impact a bond’s sensitivity to changes in spreads

Finally, credit risk and credit spread duration are often mistaken for the same thing. Mario clarifies the difference between them

Recommended